We typically have a song or two in my head. After all, watching ticks is musical and has a lot of different beats.

And typically, those songs turn into parodies.

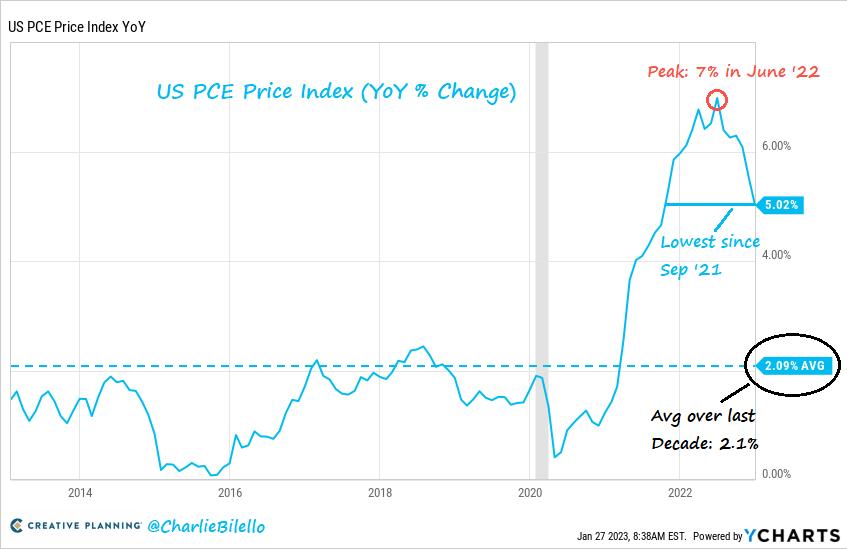

For this past week, the first song was sealed in our brains after Tesla’s extraordinary run. And then again after Friday’s PCE (Personal Consumption Expenditure) numbers were released. Core PCE excludes food and energy. PCE includes health care, education, haircuts, hospitality and more, accounts for about 50% of consumption. Powell has called it “the most important category for understanding the future evolution of core inflation.”

The first song? Reasons to be Cheerful 1,2,3 by Ian Dury and The Blockheads.

So, we got 1 (Tesla) and 2 (Softer Inflation) — what is 3?

Reason 3: Note on the chart that the Fed Funds rate is now inline with the Core PCE rate.

Powell should be doing a happy dance as this gives him the ammo to…. direct us to the next song, When Doves Cry by Prince.

However, as doves fly, so will inflation….the ultimate conundrum we have been writing about (see the Outlook 2023).

Pretty significant bounce in lumber prices. You see our dear readers, as rates soften, as Fed pauses, as markets rally, as consumers spend money, as as as…

Commodities wake up. It’s a vicious cycle. A simple economic formula of supply and demand.

Our Big View tool is invaluable in showing you the ratios among all the commodities and inflation ratios. Many raw materials remain in low supply. Copper, lithium, sugar, steel, to name a few. And speaking of sugar, on Friday, the price closed above 21 cents a pound. CANE, the Sugar Fund ETF closed on a new yearly high.

In 1972, supply shortfalls and rising demand, along with the devaluation of the dollar, all contributed to a large increase in the price of sugar. By February of 1974, with rising inflation, rising demand, and the perception of imminent shortages, sugar prices spiked to over 65¢ in November.

Now in 2023, there is speculation that smaller sugar output in India will force the country not to allow additional sugar exports. Furthermore, reduced sugar production in Europe may force European sugar and food manufacturers to import sugar, leading to tighter global supplies.

If sugar is a barometer and mirror of the 1970’s, well here’s a bonus song for you all — 1979 by Smashing Pumpkins. “That we don’t even care as restless as we are..”

Recent Dailys, along with the Outlook for 2023 go deeper into precious metals and other trading tips.

Mish’s Picks are already up 10-20% outperforming the SPY!

Want to take advantage of her stellar track record and ensure a profitable trading year? For more detailed trading information, contact Rob Quinn, our Chief Strategy Consultant, to learn more about Mish’s Premium trading service.

You don’t want to miss Mish’s 2023 Market Outlook, E-available now!

Click here if you’d like a complimentary copy of Mish’s 2023 Market Outlook E-Book in your inbox.

“I grew my money tree and so can you!” – Mish Schneider

Get your copy of Plant Your Money Tree: A Guide to Growing Your Wealth and a special bonus here.

Follow Mish on Twitter @marketminute for stock picks and more. Follow Mish on Instagram (mishschneider) for daily morning videos. To see updated media clips, click here.

Mish in the Media

Jon and Mish discuss how the market (still rangebound) is counting on a dovish Fed in this appearance on BNN Bloomberg.

Mish discusses price and what indices must do now in this appearance on Making Money with Charles Payne.

In this appearance on CMC Markets, Mish digs into her favourite commodity trades for the week and gives her technical take on where the trading opportunities for Gold, oil, copper, silver and sugar are.

Mish gives her thoughts on the big NYSE glitch on Tuesday, January 24 on this appearance for BNN Bloomberg!

Mish discusses the continued bull case for commodities and why the SPY will remain in a trading range in this appearance on Business First AM.

ETF Summary

S&P 500 (SPY): SPY has crossed the 200-DMA and is now slightly above it, but is still a very narrow price range below to 50-DMA. Held pivotal support, and now what was resistance is support at the 200-DMA and resistance is no longer 405, but 408 overhead.Russell 2000 (IWM): Filled the gap and continued to hold the 200-DMA and overhead resistance at 189 still. Closed at 189.58 resistance, now 190.66.Dow (DIA): Back over the 50-DMA and holding support at the 50-DMA; 341 is resistance still.Nasdaq (QQQ): Crossed the 50-DMA last Friday and closed above the 200-DMA and 50-DMA this Friday. First level of resistance is 299 at the 200-DMA; 200-DMA is support.Regional Banks (KRE): First level of support is 50-DMA now; it closed slightly above.Semiconductors (SMH): Still holding key support easily at the 50-WMA and 200-WMA. 237 is still support, 243 resistance.Transportation (IYT): First level of support, holding 227 with resistance at 231. Biotechnology (IBB): Still best sector, with 132 key support still holding and holding first level of support at 134 now, with 139 still resistance.Retail (XRT): Holding pivotal support at 63. First level of support at 66 resistance is still 70.

Mish Schneider

MarketGauge.com

Director of Trading Research and Education